.png?width=120&height=77&name=Summit-Virtual-CFO_color_rgb%20(1).png "Summit-Virtual-CFO_color_rgb (1)")

If you’re a service-based business with large growth goals, but no real plan to get there, you need to read this blog post.

Businesses just like yours tend to set goals like: “We’re going to increase revenue by 15% by the end of next year”. But often, service-based businesses don’t have a solid plan to execute this goal. That’s because they are missing key metrics and KPIs that will help them create a strategy.

We use profit-focused accounting when helping our clients build a plan to reach their business goals. This system was designed by our team to help clients break down revenue into financial and non-financial drivers: elements of the business that are controllable and set through SMART goals (specific, measurable, achievable, relevant, and timely). For example, to complete x number of client projects in 60 days. These drivers then assist our clients on deciding the key metrics they will need to track to determine if they are on the right track.

Note: We like to refer to metrics as levers since you can “pull” them to set you on a path towards your destination. So, if we mention a lever in the next few sections, it’s the same as a metric.

The metric categories we recommend professional services firms track include:

-

Cash

This blog post is part of a series that will cover all of the profit-focused accounting metrics listed above. For this specific blog post, we are going to go over Cash KPIs (key performance metrics) and the related levers you have at your disposal. Before we get into the details, we’d like to call out that graphics and tables are for example only. These should not be taken as industry averages.

Cash KPIs and Metrics

Cash is king. It truly is the lifeblood of a business. Without cash, a business wouldn’t be in existence. That’s why cash is a KPI category chock full of some of the most important metrics to be tracking. Let’s cover some basic cash hygiene practices before we jump into levers your business can pull to reach business goals.

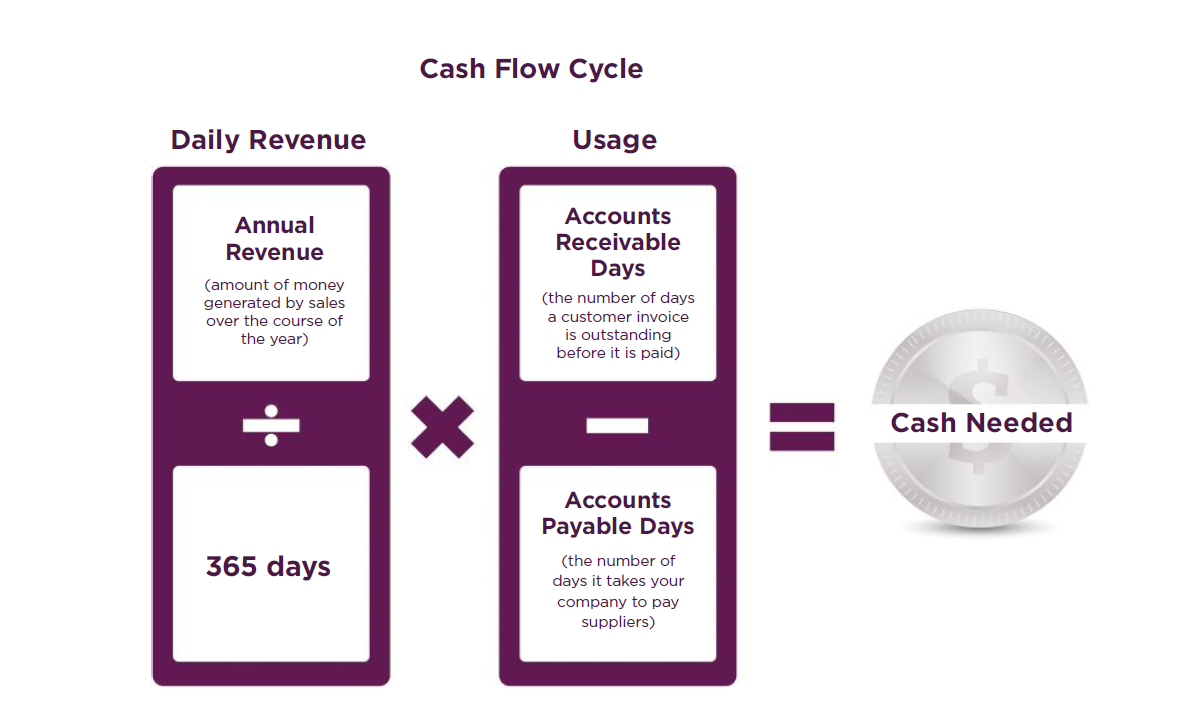

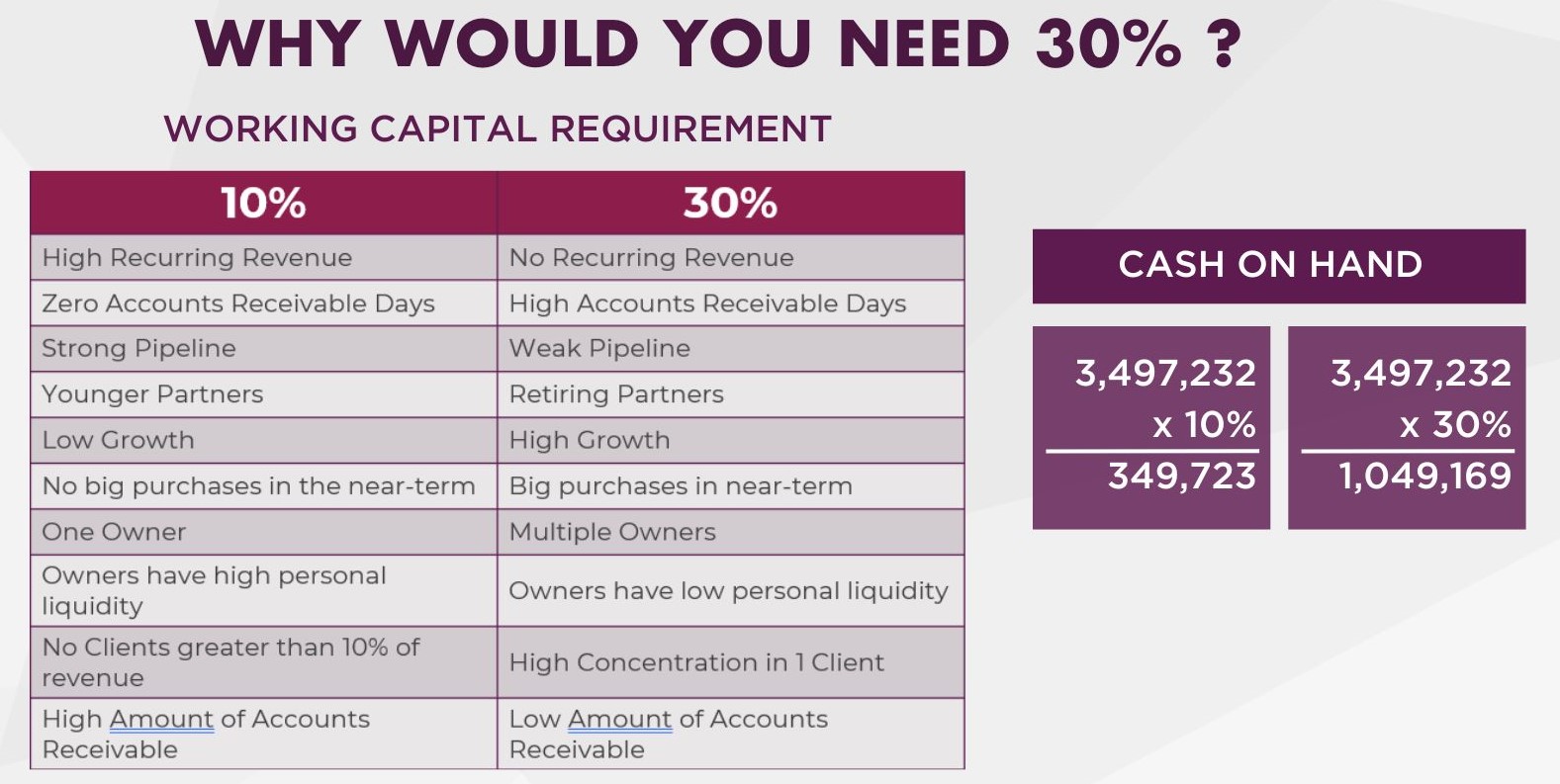

Every service-based business should keep around 10 to 30% of their yearly earnings stashed away in a cash reserve. This range is just a ballpark figure; there's actually a formula to figure out the exact cash reserve you need (check below for that formula).

The amount of cash reserves you decide to keep aside will depend on how much risk you're comfortable with. For instance, keeping 10% equals roughly two months' worth of expenses, while 30% covers about six months. Below is an example of a company earning $3,497,232 in revenue and the corresponding cash they should aim to have, based on their risk tolerance.

Businesses should have three separate bank account—an operating account, a cash reserve account, and a tax reserve account. If you can get your line of credit on a two-year cycle, that will be helpful in case of emergency or an opportunity that comes out of left field. Our quick math suggestion is to have the same amount in your line of credit as your cash reserve (if your bank will approve it).

You only want about two payrolls of cash in your operating account. The rest should be placed into your cash reserve. Putting that money in a high interest savings account, money market, or CD will keep your money safe while allowing you to generate a bit more cash off what is in the bank.

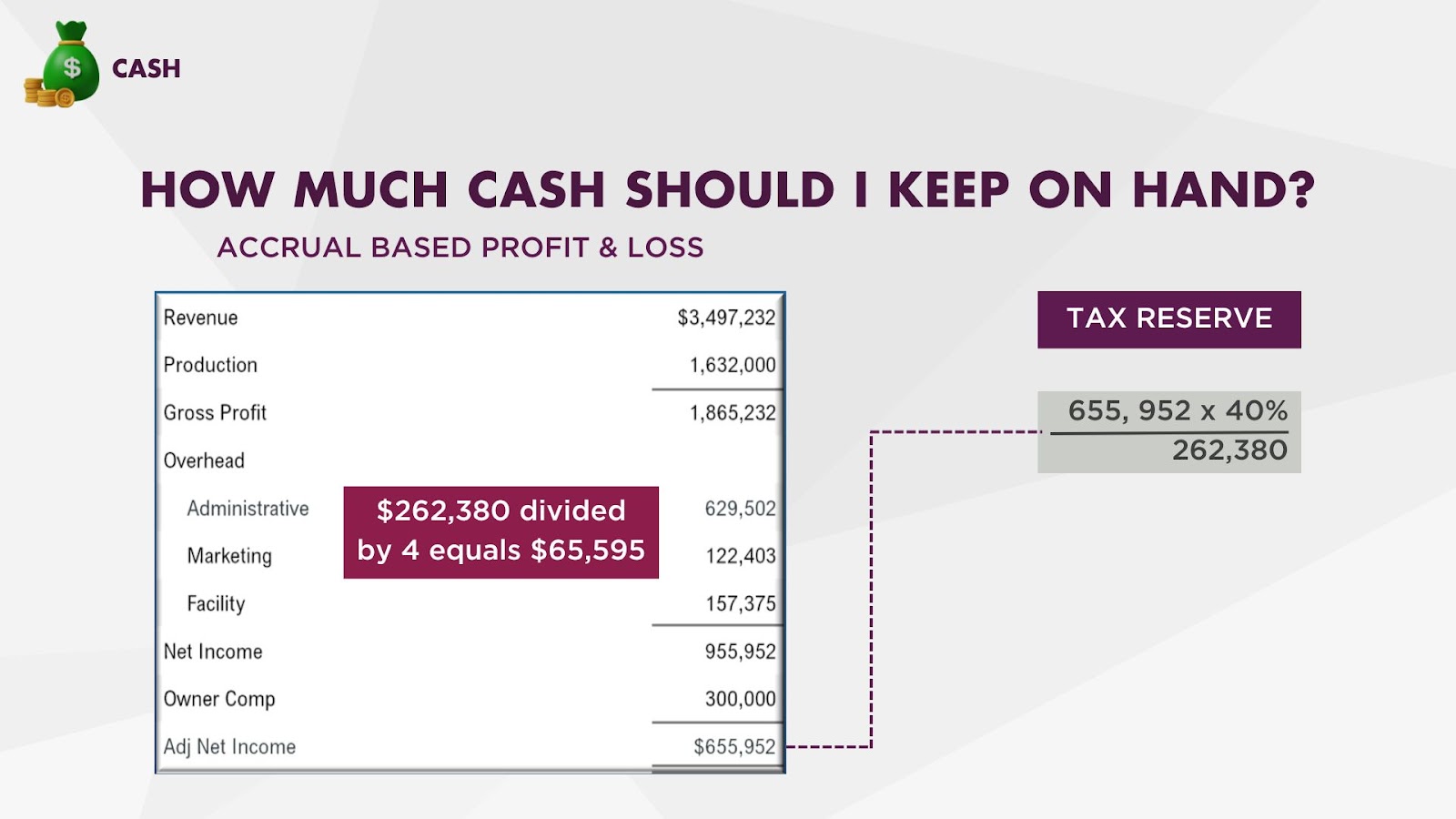

You should save 40% of your net income (your bottom line) for taxes. Put this money aside every quarter so it's out of sight and out of mind. Don't worry about a high tax bill—think of it as a sign that your business is doing well and making good profits.

Now we are ready to dig into the cash levers you have at the ready!

Improve Payment Terms

If you’re finding that you don’t have enough money to put in your cash reserve, adjusting your payment terms should be your first step. Without changing pricing or selling additional services, you can regulate business cash flow by collecting payments at a quicker pace. We’d suggest decreasing your AR (accounts receivable) days from 60 down to 15 or 30 days. By doing so, cash flow becomes more consistent, and you will no longer need to dip into your line of credit when cash is short. The below graphic gives an example of a company that ended up not needing to dip into their line of credit in March by reducing AR days to 15 days.

Collecting payments on time keeps cash flow consistent. We suggest creating a relationship with your client’s AP clerk and ensuring they have all the information they need to process payments. People are more likely to pay when they know payment due dates are tracked and missed payments are followed up accordingly. Businesses are also likely to pay on time when they have built a strong relationship with specific contacts at your company.

AR Policies

It is also worth developing an AR policy and notifying clients of what this policy entrails from the beginning. For example, you could tell clients invoices must be paid within 15 days of the issue date or there would be a consequence of pausing services if that payment is not made on time. Setting the policy is one thing, but enforcing that policy is even more important. We recommend not compromising on these terms.

This might sound intimidating to have such strict payment terms, but again, these levers are designed to generate steady cash flow for your business.

If you’d like to learn about the pipeline, financial, and production levers you can use to reach business goals, sign up for our blog notifications. We will be posting about these other levers soon.

And, if your business needs help with hitting business goals, you can sign up for a virtual CFO consultation to learn about how we help our clients set KPIs, pull levers when necessary, and set SMART goals.