.png?width=120&height=77&name=Summit-Virtual-CFO_color_rgb%20(1).png "Summit-Virtual-CFO_color_rgb (1)")

“Do I have enough cash in the bank?”

It’s one of the most common questions we hear from business owners across industries, and it’s often the thing that keeps them up at night, wondering if they can hire a new team member, afford a new major purchase or if they’ll be able to make payroll in three months’ time.

As much as accountants love certainty, there is no one right answer to that question. But we do have standard guidelines to make sure our clients have the cash to run their business, take advantage of opportunities and minimize risk.

We want cash reserves to be somewhere between 10-30% of annual revenue.

If you think about cash flow management like a road trip, that target is the fuel to help you reach your destination. You most likely won’t get there immediately – and there might be times where you decide to change your destination – but the fuel serves to let you travel toward your destination.

So how do you choose a cash reserve target? It’s a bit like deciding how much extra fuel to carry in your car. Part of it has to do with the risks inherent in your trip. What kind of business do you have? How risky is it? What is your client/customer base like? How quickly do you convert effort into cash?

Part of it depends on where you’re heading and how quickly: Are you trying to grow and scale? You’ll need more cash on hand. Are you trying to exit? Same.

And part of it depends on your comfort with uncertainty: Cash is king because it allows you to navigate factors outside of your control, like the economy. The more you have, the easier it is to bounce back from something unexpected. During the pandemic, our clients with large cash reserves were the ones who were able to accept weeks’ long shutdowns with no added stress.

A business that does $3 million in annual revenue should have anywhere from $300,000 - $900,000 in their cash reserves at all times.

Here’s how we help clients find their cash target on the 10-30% spectrum.

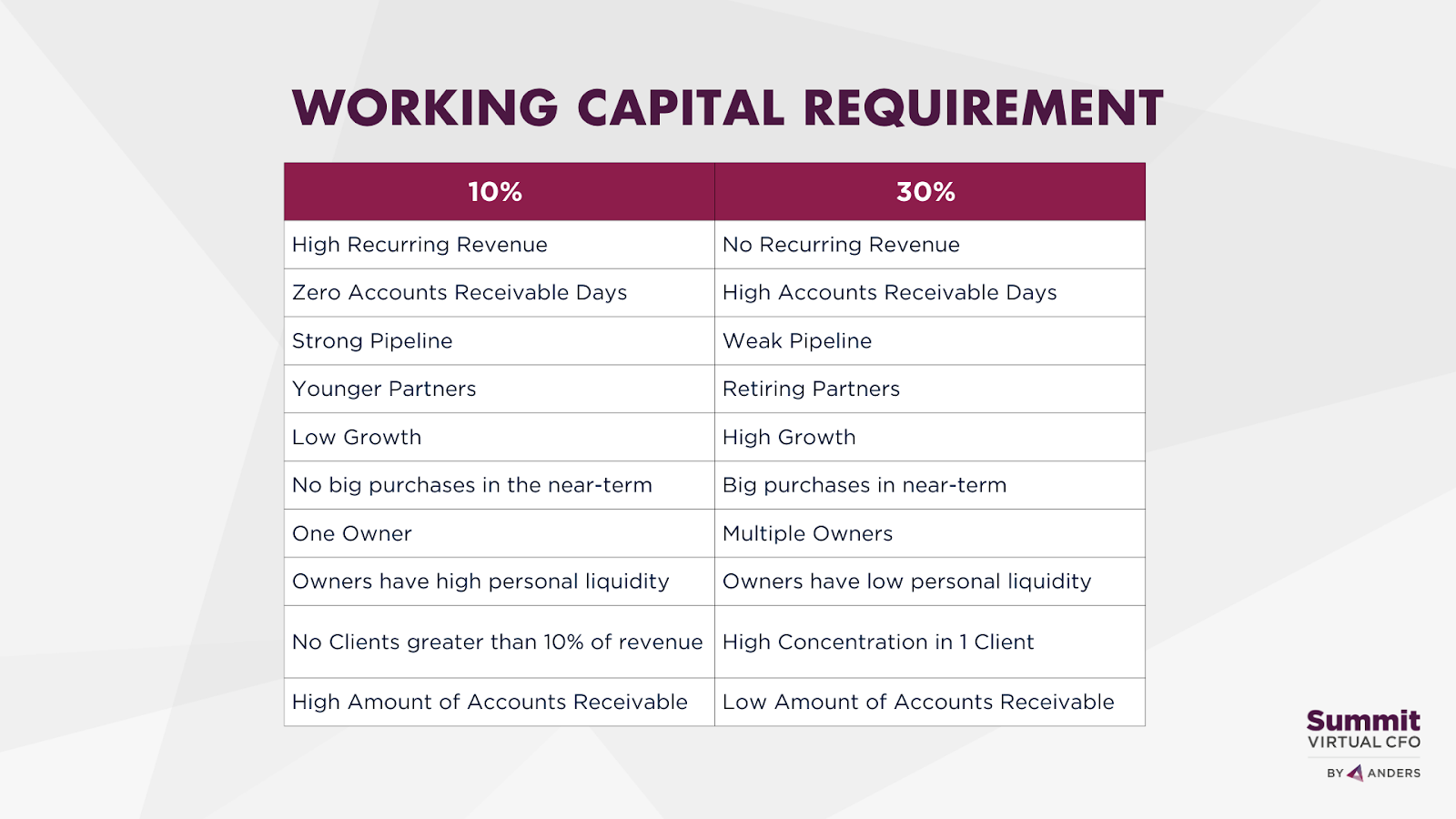

On the 10% end of the spectrum are businesses that have:

-

High recurring revenue and good billing processes with a short cash cycle. They can convert effort into cash relatively quickly without having to constantly hunt for new business.

-

A diverse client roster: they have no more than 10% of revenue from one single client and their clients are diversified across sectors.

-

Low growth; no large purchases in the near-term

-

One owner with high personal liquidity (to draw on in case of emergency); younger owners with no near-term exit plan

On the 30% end of the spectrum are businesses that have:

-

Little-to-no recurring revenue and/or a long cash cycle and poor billing practices

-

High client/customer turn-over

-

High concentration in a single client (more than 10% of revenue)

-

High growth; large purchases in the near-term

-

Multiple owners and/or low personal liquidity; owners with a near-term exit plan (requiring a costly buy-out).

Once you calculate this number, you’ll also have a good rule of thumb for the recommended size of the line of credit you should request – whether or not you actually draw on it. However, this calculation isn’t one-and-done. As these variables shift, you’ll want to revisit your goal and revise accordingly.

Remember, cash flow management is on-going. To stay on target, if revenue increases, you have to continuously increase your working capital.

5 TIPS TO OPTIMIZE CASH FLOW

A strong business model doesn’t automatically guarantee strong cash flow. But if you follow these five tips, you should be on your way to building up your reserve.

Tip #1: Keep Separate Bank Accounts to Avoid Confusion

We recommend our clients keep three separate accounts, two for working capital and one for taxes.

Keep two payrolls in the operating account, as a rule of thumb.

All additional money should stay in your reserve account, which should be interest bearing but easy access and low risk. You can move money into your operating account from your reserve account and then “repay” yourself as needed.

Tax account: You’ll want money set aside to cover quarterly estimated taxes, as we discuss below.

Tip #2: Take Taxes Off the Back Burner

Tax day should be just like any other day of the year. If you’re setting aside 40% of your forecasted taxable income in a separate tax account on a weekly or monthly basis – beyond the cash reserve amount – and making your estimated payments based on the prior year, there’s no reason to be caught off guard. With tax money in a separate account, you won’t be tempted to spend it or get a false sense of security.

Tip #3: Improve Billing Hygiene

Good cash flow starts with timely billing, because the faster you convert effort into dollars, the healthier your business will be.

Every new client or customer relationship should begin with clear billing policies – consider making it part of your onboarding process. You may want to experiment with shortening payment terms, even by as little as 15 days. Other ways to boost billing hygiene include instituting retainers or larger deposits/down payments.

Billing software can boost your collection efficiency, allowing you to email invoices, check open rates and send reminders. A 30-day delay on an unpaid invoice will have a noticeable impact on cash flow.

Tip #4: Use Your Forecasts Wisely

A successful business with no forecast is a lucky business – but luck runs out. The best way to stay ahead of the curve is to create and update your forecast on a regular (monthly!) basis.

A forecast that sits on a hard drive for a year is not really a forecast. It’s a bit like having a paper map for a road trip instead of using a GPS: a dynamic forecast will allow you to adjust to understand the implications of any major changes to your business. You might have an opportunity to make an acquisition, introduce a new service line, or hire top talent. You might lose a major client or face an industry downturn. A forecast will help you stay on top of these changes and give you real-time insights along the way.

This is just a high-level overview of one of the metrics of profit-focused accounting: cash. To get regular insights on best financial practices for small business owners, subscribe to our newsletter or to find out how we can help your business specifically, schedule a complimentary consultation now.

Tip #5: Separate Duties for Reconciling Books

Solution: Use three different people to issue/record, review and reconcile payments.

In a small business, if the same person is doing too many different jobs, you can end up making mistakes – or becoming the victim of fraud. The best cash flow practices involve three different people to handle each phase:

-

A bookkeeper who prepares disbursements and receive payments

-

An owner or manager who reviews and approves payments

-

A third-party who reconciles the accounts

Separating duties is the surest way to avoid fraud. But, it also leads to better quality, more timely financials, by dividing the labor: It’s a lot of work to oversee cash receipts, cash disbursements, recording and reconciling, especially if the sole person responsible also has other duties.

If you'd like to see how we help our clients improve profitability by optimizing their cash flow strategy, check out our virtual CFO services below.